AHA Center for Health Innovation Market Scan

Hospitals and health systems have a growing list of competitors to concern themselves with as they navigate relationships with physician practices.

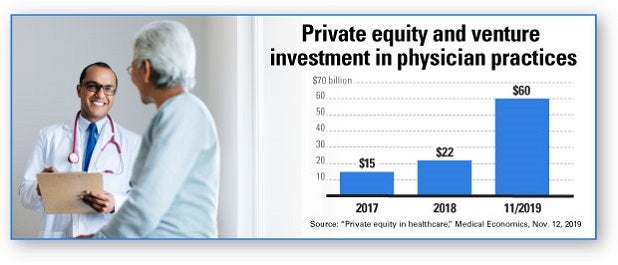

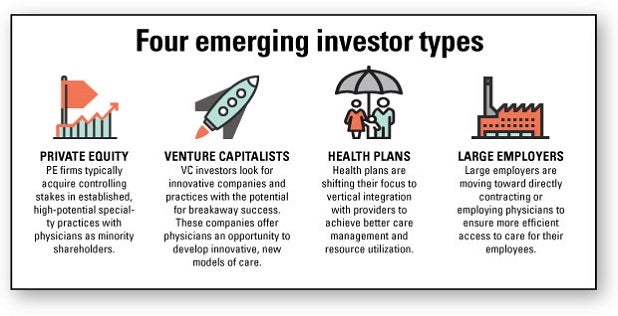

Nontraditional players, including private equity and venture capital firms, health plans and large employers increasingly are targeting physician practices for investment. Private equity investor deals in the U.S. related to physician practices in 2018 totaled $22 billion. By November 2019, that figure had surged to $60 billion and shows no sign of abating, Medical Economics reports.

This trend has left some hospitals and health systems feeling uncertain as their longtime partners draw investments from organizations that may have divergent interests.

A new AHA Center for Health Innovation Market Insights Report “Evolving Physician-Practice Ownership Models” explores the role of physicians at the center of the health care value equation, analyzes emerging investor types, strategic implications for hospitals and health systems and organizational threats and opportunities. In addition, several experts from firms that partner with hospitals and health systems and physician practices share their insights on what’s shaping trends in physician-practice ownership models.

UnitedHealth Group, Aetna, various Blue Cross Blue Shield entities and others now offer plans built around clinics the insurers or their affiliate companies own, featuring smaller networks with more limited choices of doctors and hospitals. This can reduce premiums, but insurers also benefit because they keep revenues inside their holdings. “Suddenly, the plan you’re relying on for payment is also competing with you at the front end of the delivery system,” Chas Roades, a health care consultant, recently told the Wall Street Journal.

While the impact of these trends will be highly market dependent, there are some significant business implications for hospitals and health systems to consider. Some include:

If investors are able to execute innovative new models of care, streamline operations and expand the continuum of physician practices, this also could create opportunities to partner or affiliate.

With this in mind, hospitals and health systems need to develop thoughtful and targeted physician alignment strategies based on organizational goals, available resources, practice management competencies and local market conditions. Regardless of the options for physician alignment, strong physician leadership and integration into practice governance models are key ingredients for success.

For hospitals and health systems evaluating their strategies related to physician alignment, the report cites five organizational opportunities to consider, including:

As companion pieces to the new “Evolving Physician-Practice Ownership Models” report, the AHA Center for Health Innovation has launched the following new resources:

![]()