Testimony

After three years of unprecedented challenges and caring for millions of patients, including over 6 million COVID-19 patients, America’s hospitals and health systems are facing a new existential challenge — sustained and significant increases in the costs required to care for patients and communities putting their financial stability at risk.

A confluence of several factors from historic inflation driving up the cost of medical supplies and equipment, to critical workforce shortages forcing hospitals to rely heavily on more expensive contract labor, led to 2022 being the most financially challenging year for hospitals since the pandemic began. Moreover, sustained demand for hospital care with patients coming to the hospital sicker and staying longer has exacerbated these challenges.

These challenges have been particularly financially devastating for hospitals and health systems because they come on top of two years of battling the COVID-19 pandemic. Hospitals and health systems have been on the front lines delivering care to patients, acting as de facto public health agencies, and incurring significant increases in costs from a range of inputs, including labor, drugs, supplies and administrative activities associated with burdensome billing and insurance tasks. In addition, as many individuals deferred care during the pandemic, hospitals saw a dramatic rise in patient acuity. At the same time, workforce shortages across the health care continuum have left hospitals unable to discharge patients to other care settings (e.g., skilled nursing facilities) creating patient bottlenecks with hospital beds occupied without any reimbursement.

These challenges have been particularly financially devastating for hospitals and health systems because they come on top of two years of battling the COVID-19 pandemic. Hospitals and health systems have been on the front lines delivering care to patients, acting as de facto public health agencies, and incurring significant increases in costs from a range of inputs, including labor, drugs, supplies and administrative activities associated with burdensome billing and insurance tasks. In addition, as many individuals deferred care during the pandemic, hospitals saw a dramatic rise in patient acuity. At the same time, workforce shortages across the health care continuum have left hospitals unable to discharge patients to other care settings (e.g., skilled nursing facilities) creating patient bottlenecks with hospital beds occupied without any reimbursement.

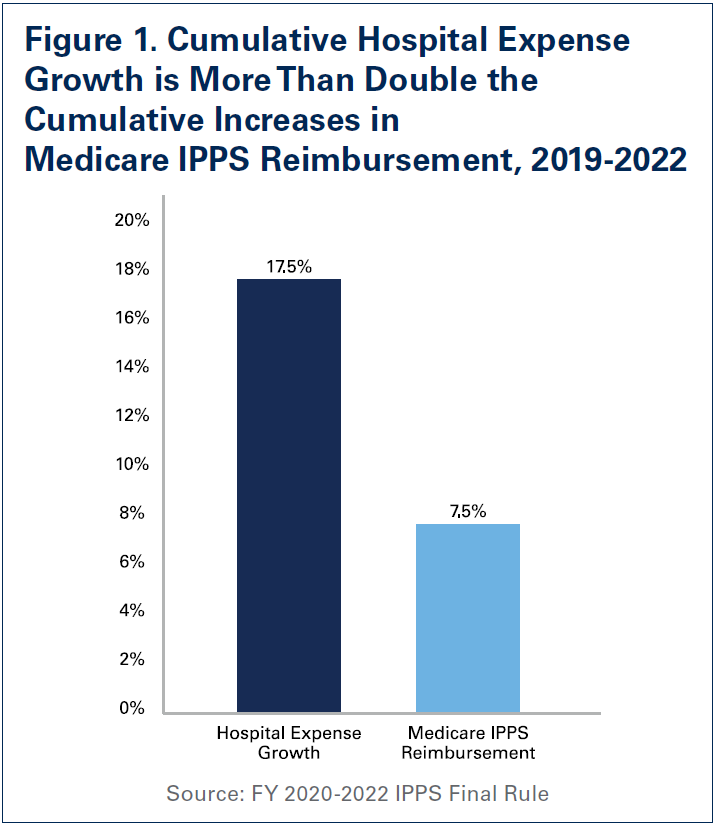

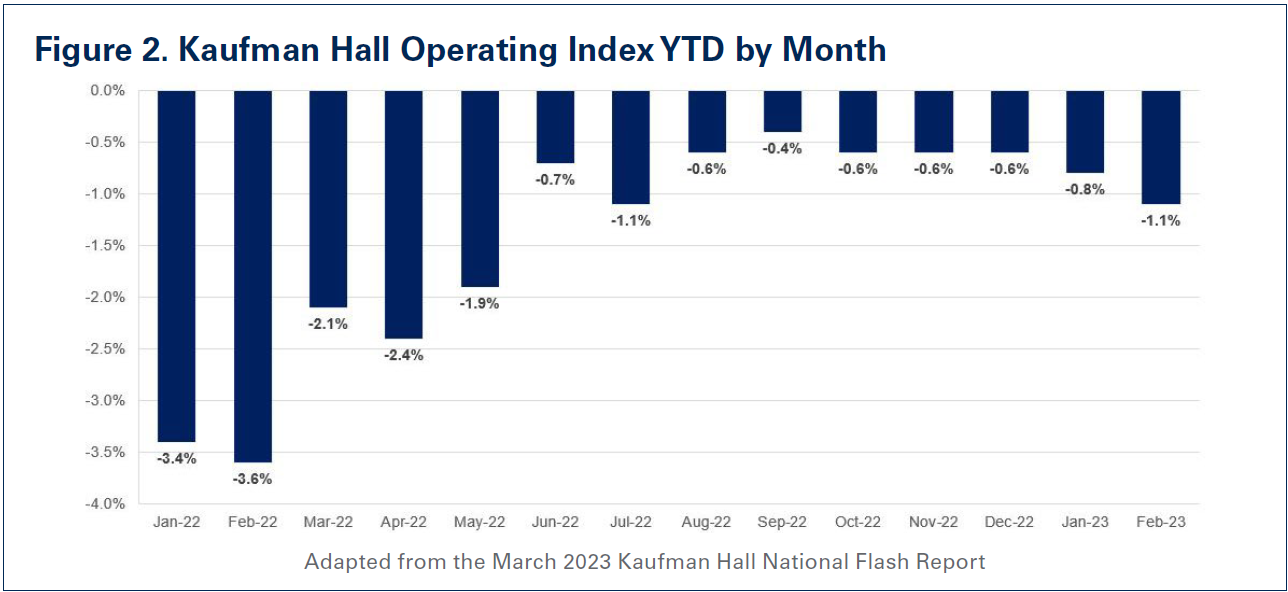

These unfortunate realities have resulted in a 17.5% increase in overall hospital expenses between 2019 and 2022, according to data from Syntellis Performance Solutions, a health care data and consulting firm. Further exacerbating the situation is the fact that the staggering expense increases have been met with woefully inadequate increases in government reimbursement. Specifically, hospital expense increases between 2019 and 2022 are more than double the increases in Medicare reimbursement for inpatient care during that same time (See Figure 1). Because of this, margins have remained consistently negative, according to Kaufman Hall’s Operating Margin Index throughout 2022 (See Figure 2). In fact, over half of hospitals ended 2022 operating at a financial loss — an unsustainable situation for any organization in any sector, let alone hospitals. So far, that trend has continued into 2023 with negative median operating margins in January and February. According to a recent analysis, the first quarter of 2023 saw the highest number of bond defaults among hospitals in over a decade.1 This also is one of the primary reasons that some hospitals, especially rural hospitals, have been forced to close their doors. Between 2010 and 2022, 143 rural hospitals closed — 19 of which occurred in 2020 alone.2,3 Finally, despite these cost increases, hospital prices have grown modestly. In fact, in 2022, growth in general inflation (8%) was more than double the growth in hospital prices (2.9%).

This report will examine the magnitude of cost increases over the last year, and the impact these increases have had on the financial stability of the hospital field.

Beginning in early 2022, the hospital field's existing workforce shortages were exacerbated with increased patient demand for hospital care due to a combination of sustained COVID-19 surges, a new virulent disease affecting primarily pediatric patients called respiratory syncytial virus (RSV), and deferred care from the early days of the pandemic. To quickly meet this demand, hospitals were increasingly forced to turn to health care staffing agencies to fill necessary gaps, especially for bedside nursing and other critical allied health professionals such as respiratory and imaging technicians.

Labor has been really the primary driver of our increased expenses. We've seen a 17% increase in our nursing costs, for instance, during COVID, mainly because of many nurses leaving the field and the workforce. — President and CEO of a health system in the Northeast

A recent report by Syntellis Performance Solutions found that full-time equivalents (FTEs) for hospital contract employees jumped 138.5%. This reliance on temporary contract labor came at a significant expense to hospitals, as health care staffing agencies took advantage of the situation and increased their rates to record high levels. The same report found that the rate hospitals were charged for contract employees increased 56.8% in 2022 compared to pre-pandemic levels. It is for this reason that hospitals’ contract labor expenses increased a staggering 257.9% in 2022 relative to 2019 levels (See Figure 3).

The explosive growth in contract labor expenses in large part fueled the 20.8% increase in overall hospital labor expenses during the same time period. Even after accounting for the fact that patient acuity (as measured by the case mix index) has increased during this period, labor expenses per patient increased 24.7%. These increases are particularly challenging, because labor on average accounts for about half of a hospital's budget.

The historic rise in inflation has been particularly challenging for hospitals and health systems as it has sparked a significant increase in non-labor expenses. As prices for essential goods such as food and clothing have seen significant price growth, so too have the prices for essential goods for hospitals such as drugs and medical supplies.4 A report by Kaufman Hall estimated that non-labor expenses alone would result in a one-year expense increase of $49 billion for hospitals and health systems.5,6 In fact, since 2019, non-labor expenses have increased 16.6% on a per patient basis. Below, we focus on three areas of non-labor expenses that have seen tremendous cost growth:

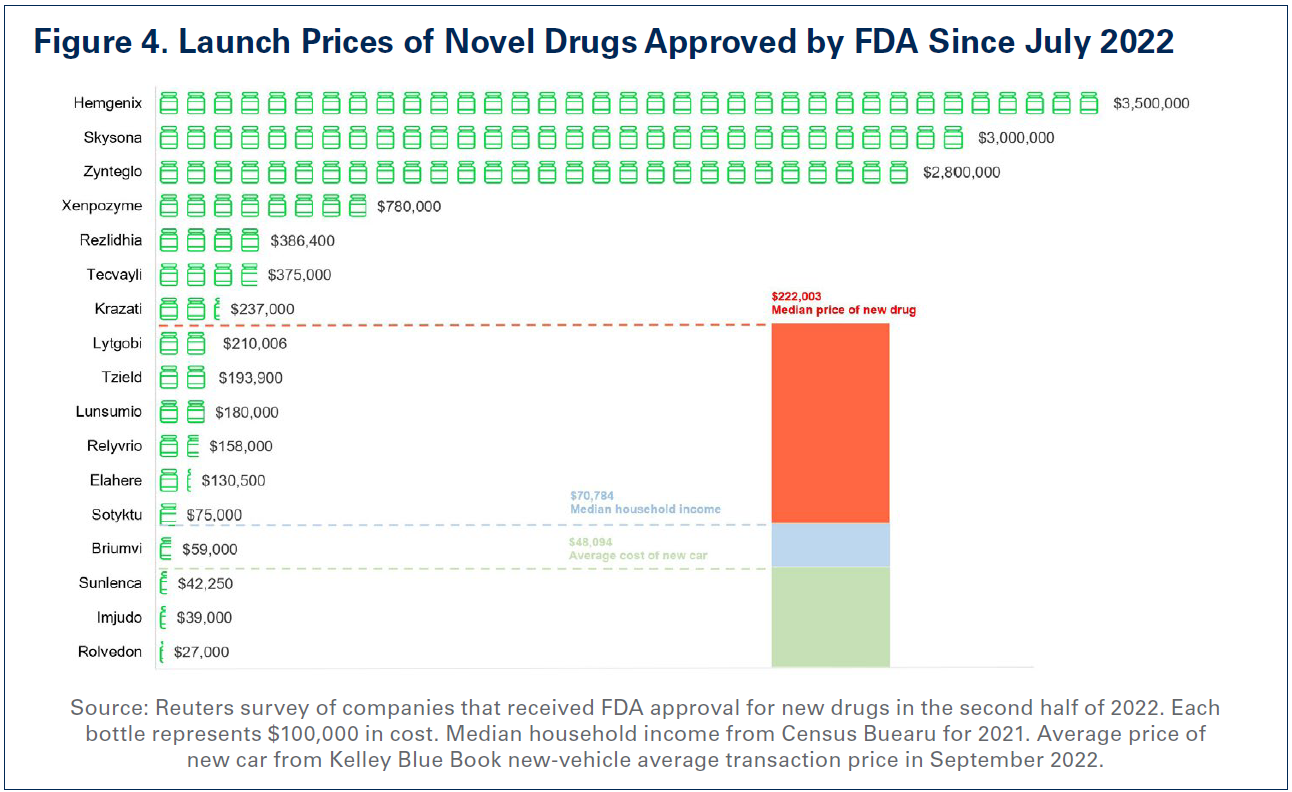

As hospitals and health systems faced an increasingly challenging environment due to pandemic surges as well as workforce shortages, drug companies took the opportunity to significantly raise the prices of existing drugs as well as introduce new drugs at record prices.7 High drug prices affect both patients directly and hospitals, especially when purchasing provider-administered drugs. In fact, for the first time in history, the median price of a new drug exceeded $200,000 — a staggering figure that implies a double-digit year-over-year price growth (See Figure 4).8,9 To further contextualize these launch prices, the median new drug launch price is more than quadruple the average price of a new car and more than triple the median annual household salary ($70,784) in the United States, illustrating how unaffordable these drugs are for both providers and their patients.10

In addition, a report by the Assistant Secretary for Planning & Evaluation (ASPE) at the Department of Health and Human Services (HHS) found that drug companies increased drug prices for 1,216 drugs — many used to treat chronic conditions like cancer and rheumatoid arthritis — by more than the rate of inflation, which was 8.5% between 2021 and 2022. In fact, the average price increase for these drugs was 31.6%, with some drugs experiencing price increases as much as 500%.11 Moreover, recent drug shortages, specifically for certain drugs used to treat cancer, have also fueled further expense growth. It is estimated that drug shortages alone cost hospitals nearly $360 million a year.12

Therefore, it is no surprise, that as hospitals face the reality of operating on negative margins, drug companies are enjoying record revenues and profits. For example, some drug companies are experiencing over 200% revenue growth.13

"In the last year, we've seen double digit increases in pharmaceuticals and medical supplies. Our utility costs are up and certainly our labor costs are up." — CEO of a health system in the South

For these reasons, high drug prices have been a primary driver of skyrocketing drug costs for hospitals. According to data from Syntellis Performance Solutions, hospital drug expenses per patient have increased 19.7% between 2019 and 2022. Even after accounting for the fact that patients were on average sicker (as measured by the case mix index) in 2022 than in 2019, drug expenses per patient were up over 18%. This suggests that the growth in hospital drug expenses is not primarily due to sicker patients requiring more drugs, rather it is a result of drug companies’ deliberate decisions to increase the prices of their products.

While the demand for patient care has risen, so has the need for medical supplies necessary to deliver patient care and personal protective equipment (PPE) necessary to ensure the safety of both hospital staff and patients. Hospitals rely on a global supply chain for access to these supplies and equipment, and entities across the supply chain have experienced inflationary cost increases. Ongoing supply chain disruptions have led to higher manufacturing costs, packaging costs, and shipping costs, which translate into higher prices for hospitals.14 In fact, the National Academies recently released a report highlighting the ongoing challenges that supply chain disruptions place on providers needing to access medical supplies.15

"But in other industries like we see in our area, manufacturing, retail, hospitality, you can decide not to fill that order. You can decide to shut your restaurant down for a day. We can't do that in health care." — President and CEO of a health system in the Midwest

As a direct result, hospital supply expenses per patient increased 18.5% between 2019 and 2022, outpacing increases in inflation by nearly 30%. Particularly alarming is the growth in supply costs needed for care in the emergency department — often the first level of care provided in the hospital. Hospital expenses for emergency services supplies experienced a nearly 33% increase between 2019 and 2022. These include equipment such as ventilators, respirators and other sophisticated equipment that are critical to keeping patients alive in the emergency department. As patient acuity has increased dramatically during this period, the need for these equipment to care for more complex patients also has increased.16 More specifically, as patients stay in the hospital longer requiring more intensive care, the amount of supplies and the type of supplies required to care for those patients become more expensive.17

In addition to hospitals’ costs for drugs and medical supplies and equipment, costs for other areas that help support patient care such as purchased service expenses also have risen precipitously. This, in part, has driven clinical costs higher, making clinical services such as emergency and lab services more expensive to administer.

In addition to hospitals’ costs for drugs and medical supplies and equipment, costs for other areas that help support patient care such as purchased service expenses also have risen precipitously. This, in part, has driven clinical costs higher, making clinical services such as emergency and lab services more expensive to administer.

Purchased service expenses, which are expenses hospitals incur to create operational efficiencies such as information technology (IT), environmental services and facilities, and food and nutrition services increased 18% between 2019 and 2022. With increased patient demand and inflationary pressures, hospitals have been forced to incur additional purchased service costs as they renew and renegotiate their purchased service contracts. For example, as the cost of food has gone up over the last year, hospitals’ food services costs have grown. Specifically, food and nutrition service expenses per patient grew over 15% between 2019 and 2022.

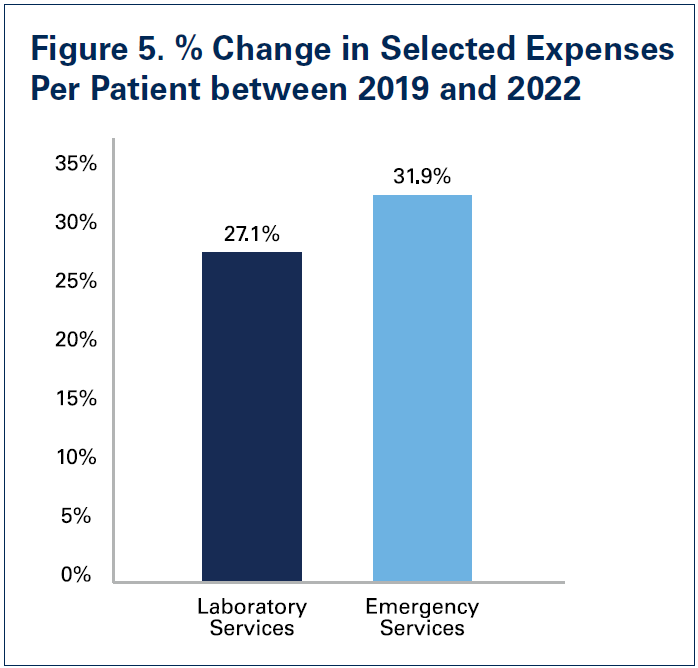

Hospitals also have incurred increased costs in particular clinical areas. This is due to a combination of increased patient demand after many patients delayed or avoided care during the pandemic and inflationary cost growth for supplies and equipment needed to provide care. Specifically, compared to 2019 levels, laboratory service expenses per patient were up 27.1% in 2022 and emergency service expenses per patient were up 31.9%.

With hospitals bearing cost growth in many areas, they have been forced to cut costs elsewhere to stay financially afloat, and in the case of many rural hospitals, simply keep the doors open.

Notwithstanding labor and non-labor expense increases, commercial health insurer policies like unnecessary prior authorization requirements and improper claim denials continue to add significant burden for hospital staff — diverting staff time from caring for patients and contributing to clinician burnout. These practices add substantial administrative costs to the health care system by slowing down the provision of care, requiring providers to purchase additional IT tools to manage insurer requirements and necessitating the hiring of additional staff solely to manage administrative paperwork.

Administrative costs constitute as much as 31% of total health care spending — 82% of which can be attributed to billing and insurance.18 In a recent survey fielded by the AHA, 84% of hospitals reported the cost of complying with insurer policies is increasing, with 95% reporting increases in time spent seeking prior authorization approval.19 Even though more than half of all prior authorization denials are overturned, commercial health insurers continue to flood hospitals with prior authorization denials to the detriment of both patients and providers. This is especially egregious when prior authorization is required for widely available lifesaving medications with clear clinical indications for use, such as insulin, where the service or treatment protocol are neither new nor have a history of unwarranted variation in utilization. The AHA report also found that 50% of hospitals and health systems have more than $100 million in accounts receivables for claims that are older than six months, which impact hospitals’ cash flow and ability to weather the avalanche of cost increases they have faced. Shockingly, seven in 10 hospitals reported having an outstanding claim from 2016 or older. In addition, 35% of hospitals reported $50 million or more in foregone payments because of denied claims.

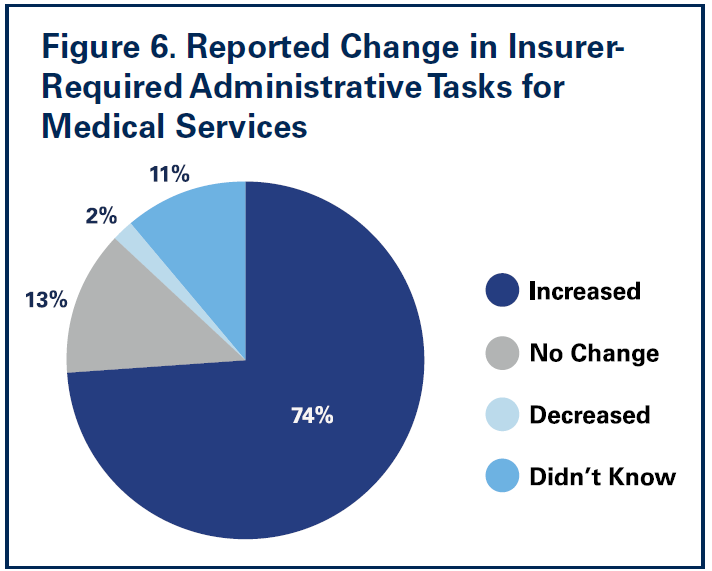

A recent survey conducted by Morning Consult on behalf of the AHA found that nearly three-fourths of nurses reported increases in insurer-required administrative tasks for medical services over the last five years. Nearly 9 in 10 nurses reported insurer administrative burden had negatively impacted patient clinical outcomes (See Figure 6 on next page).

A recent survey conducted by Morning Consult on behalf of the AHA found that nearly three-fourths of nurses reported increases in insurer-required administrative tasks for medical services over the last five years. Nearly 9 in 10 nurses reported insurer administrative burden had negatively impacted patient clinical outcomes (See Figure 6 on next page).

Confronted by ever-growing costs, hospitals have been limited in how they can respond to the administrative burden levied by commercial health plans. Over the course of the last several years many hospitals, looking for operational efficiencies to combat rising costs, have been driven to trim down their administrative workforce.20 However, with a narrowing menu of options for hospitals to choose from in responding to insurer administrative expenses, 78% of hospitals report their experience with commercial health insurers is getting worse.

As the public health emergency comes to end on May 11, a number of important waivers and flexibilities also will come to an end immediately, or will sunset at the end of this year.21 The downstream effects of this will be wide-ranging as hospitals will be faced with a set of additional challenges. For example, with the end of the public health emergency, the continuous Medicaid enrollment provision will no longer be in effect starting April 1 meaning that states can begin dis-enrolling current Medicaid beneficiaries from the program that do not meet the state’s Medicaid enrollment criteria. According to the Kaiser Family Foundation, as many as 14 million current Medicaid beneficiaries could lose coverage over the next year.22 Undoubtedly, these coverage losses will drive higher rates of uninsured and underinsured individuals, raising hospitals’ uncompensated care costs and potentially negatively impacting disproportionate share payments as well as 340B program eligibility, both of which allow hospitals to offset some of the expense increases as well as furnish programs and services critical to patients. Further, the ending of regulatory relief through the 20% Medicare inpatient prospective payment system add-on payment for beneficiaries diagnosed with COVID-19 to offset the cost of highly complex care for these patients, will certainly add financial pressure to an already fragile situation for hospitals and health systems.

The combination of the impacts on hospitals of the ending public health emergency as well as continued expense growth has created an uncertain future for hospitals and health systems. A study by McKinsey on the impact of inflation and other cost pressures for the health care system projected that there would be $98 billion in additional costs between 2022 and 2023 alone, representing an astounding $248 billion increase in costs relative to 2019.23 In fact, their projections suggest that non-labor costs alone could increase by $112 billion by 2027. Therefore, it is no surprise, that credit rating agencies have a negative outlook for the field. For example, Moody’s has projected a negative outlook for the hospital field for 2023 due in large part to inflationary cost pressures and persisting workforce challenges.24

Hospitals and health systems — and their teams — are committed to providing high-quality care to all patients in every community. This steadfast commitment to caring and advancing health has never been more apparent than during the last three years battling the greatest public health crisis in a century.

However, the costs of delivering on this commitment to care have grown tremendously. As the data in this report show, 2022 brought an unprecedented set of challenges for hospitals and health systems, which has left the field in a financially unsustainable situation. These challenges are continuing in 2023.

To address these challenges and ensure hospitals have the ability to continue taking care of the sick and injured, as well as keeping people and communities healthy, congressional support and action are necessary. Among other actions, Congress should:

As the hospital field maintains its commitment to care in the face of significant challenges, policymakers must step up and help protect the health and well-being of our nation by ensuring America has strong hospitals and health systems.