Testimony

Who’s Really Driving Physician Acquisitions?

The Outsized Role of Commercial Insurers and Corporate Entities

Commercial insurers and corporate entities continue to play an outsized role in reshaping the physician acquisition landscape, overshadowing hospitals’ role in these deals. A new AHA analysis of data from LevinPro HC covering nearly 800 physician practice acquisitions between 2019 and 2024, reveals that commercial insurers and corporate entities like Amazon continue to lead acquisitions, with a particular emphasis on acquiring higher-margin, scalable specialties in densely populated markets rather than lower-margin specialties. These data provide further evidence that commercial insurers and corporate entities may base acquisition decisions on different motivations than hospitals and health systems, which are more likely to be involved in deals with lower-margin specialties that ensure continued access to essential services to communities.

Key Findings from the AHA Analysis:

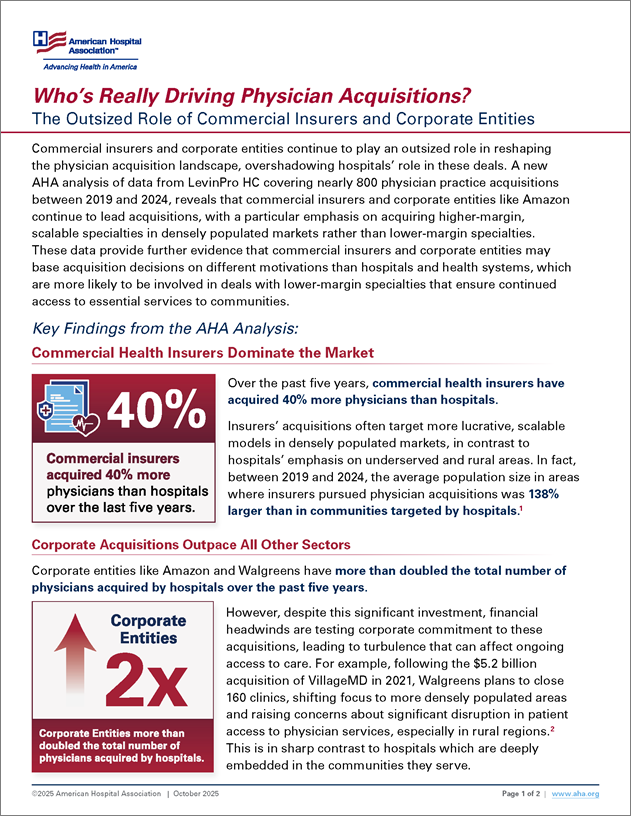

Commercial Health Insurers Dominate the Market

Over the past five years, commercial health insurers have acquired 40% more physicians than hospitals.

Insurers’ acquisitions often target more lucrative, scalable models in densely populated markets, in contrast to hospitals’ emphasis on underserved and rural areas. In fact, between 2019 and 2024, the average population size in areas where insurers pursued physician acquisitions was 138% larger than in communities targeted by hospitals.1

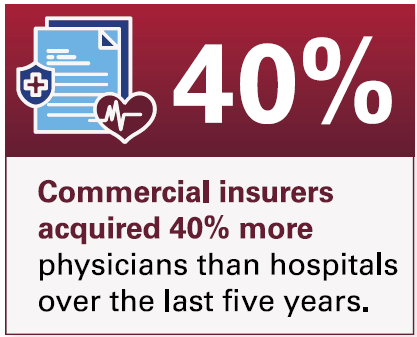

Corporate Acquisitions Outpace All Other Sectors

Corporate entities like Amazon and Walgreens have more than doubled the total number of physicians acquired by hospitals over the past five years.

However, despite this significant investment, financial headwinds are testing corporate commitment to these acquisitions, leading to turbulence that can affect ongoing access to care. For example, following the $5.2 billion acquisition of VillageMD in 2021, Walgreens plans to close 160 clinics, shifting focus to more densely populated areas and raising concerns about significant disruption in patient access to physician services, especially in rural regions.2 This is in sharp contrast to hospitals which are deeply embedded in the communities they serve.

However, despite this significant investment, financial headwinds are testing corporate commitment to these acquisitions, leading to turbulence that can affect ongoing access to care. For example, following the $5.2 billion acquisition of VillageMD in 2021, Walgreens plans to close 160 clinics, shifting focus to more densely populated areas and raising concerns about significant disruption in patient access to physician services, especially in rural regions.2 This is in sharp contrast to hospitals which are deeply embedded in the communities they serve.

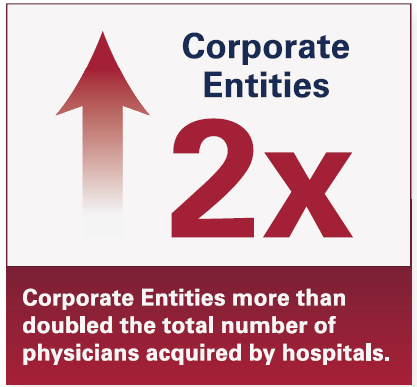

Hospitals’ Focus on Maintaining Primary Care Services

Hospitals accounted for 94% of acquired physicians in lower-margin specialties like pediatric medicine and less than 3% of physicians in higher-margin specialties like dermatology, gastroenterology, and cardiology.

In fact, 71% of all physicians acquired by hospitals were in family medicine or pediatric medicine between 2019 and 2024, indicating hospitals’ focus on providing access to essential care in primary and pediatric specialties.

__________

1 Physician group characteristics from Definitive Healthcare.

2 aha.org/aha-center-health-innovation-market-scan/2024-04-09-walgreens-shutters-160-villagemd-clinics-after-6-billion-loss